Managament Stock-options Valuation

Valuation

© Constency Publishing | LesEchos Finance

12/9/20131 min read

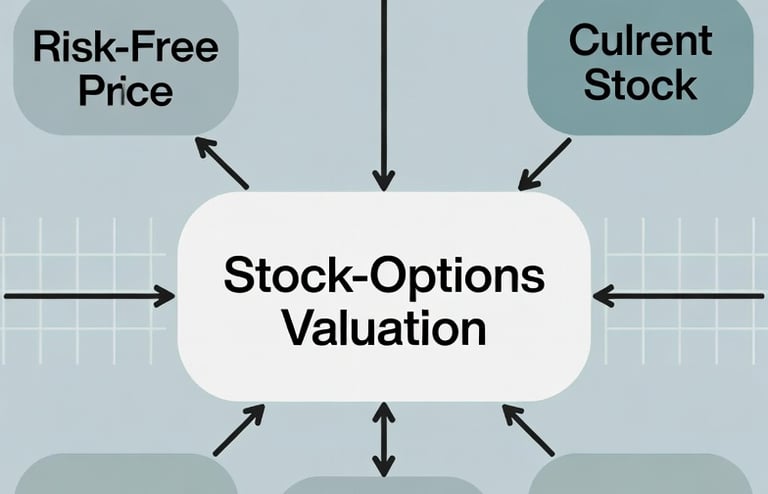

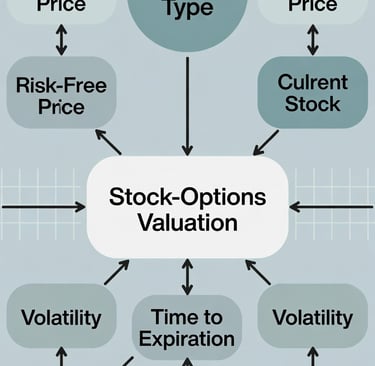

Management stock-options are not traded, their fair value must be calculated by models able to reflect their particular characteristics. They have specific features to deal with.

As market prices don’t exist for such instruments, their fair value is determined by applying a suitable valuation technique.

Valuation will combine the use of (i) an option pricing model and (ii) specifics considerations that will reflect their features. The three most common option pricing models are the Black-Scholes, binomial, and Monte Carlo simulation.

In the context of a LBO, several factors will affect the valuation of a typical nontraded management stock-options, such as vesting features and behavioral considerations.

Significant variation in the valuation results

Defining the assumptions and estimates in the valuation model are fundamentals. The reliability of a fair value determination is especially affected by the factors level. Any variation used in the model will lead to significant variation in the results of the valuation.

Companies specificities

It may be appropriate to use separate models for different companies to reflect their business industry and markets. Specific models may be necessary to deal with issues that require complex consideration.

For Biotech companies, we can mention the following specificities:

The ratio of R&D to sales is very high at around 25% of revenue.

The development process requires more than 15 years with high risks of failure during all the process.

Entities should engage a valuator to determine the value of Management stock-options, so that they can issue options that don’t create tax issues and that satisfy the fair value.

This article was first published on Capital Finance - LesEchos - 2013

Constency

© 2025. Constency Global. All rights reserved.

Constency is the brand used by independent audit and consulting firms, each of which is a separate and independent legal entity. Each firm and related entity cannot obligate or bind each other in respect of third parties. Each firm and related entity is liable only for its own acts and omissions, and not those of each other.